AI Is Eating Upwork From the Bottom Up. It Might Also Save It.

A dive into whether AI is truly disrupting digital labor marketplaces like Upwork and Fiverr as much as the news headlines might suggest.

Hi, it’s Colin! Welcome to the 220 new subscribers who have joined Take Rate since the last post. I am excited to have you join the 5,160+ marketplace founders, operators, and investors who subscribe. Join the fun! 👇

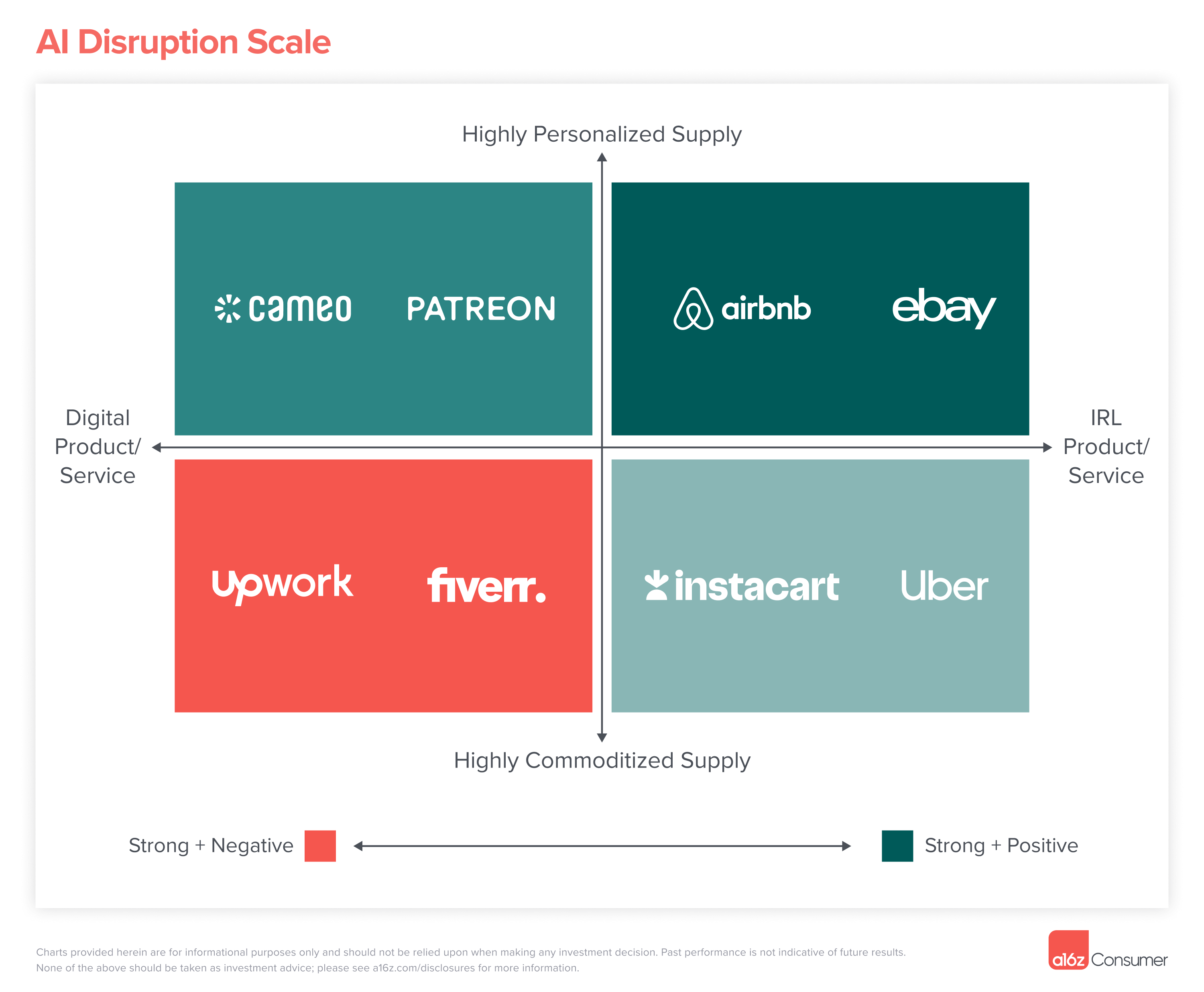

For a while, I’ve assumed Upwork would be one of the first companies hit hardest by AI. The logic seemed obvious. A marketplace built on small, well-scoped, commoditized, remote, and digital tasks is the kind of work LLMs eat first.

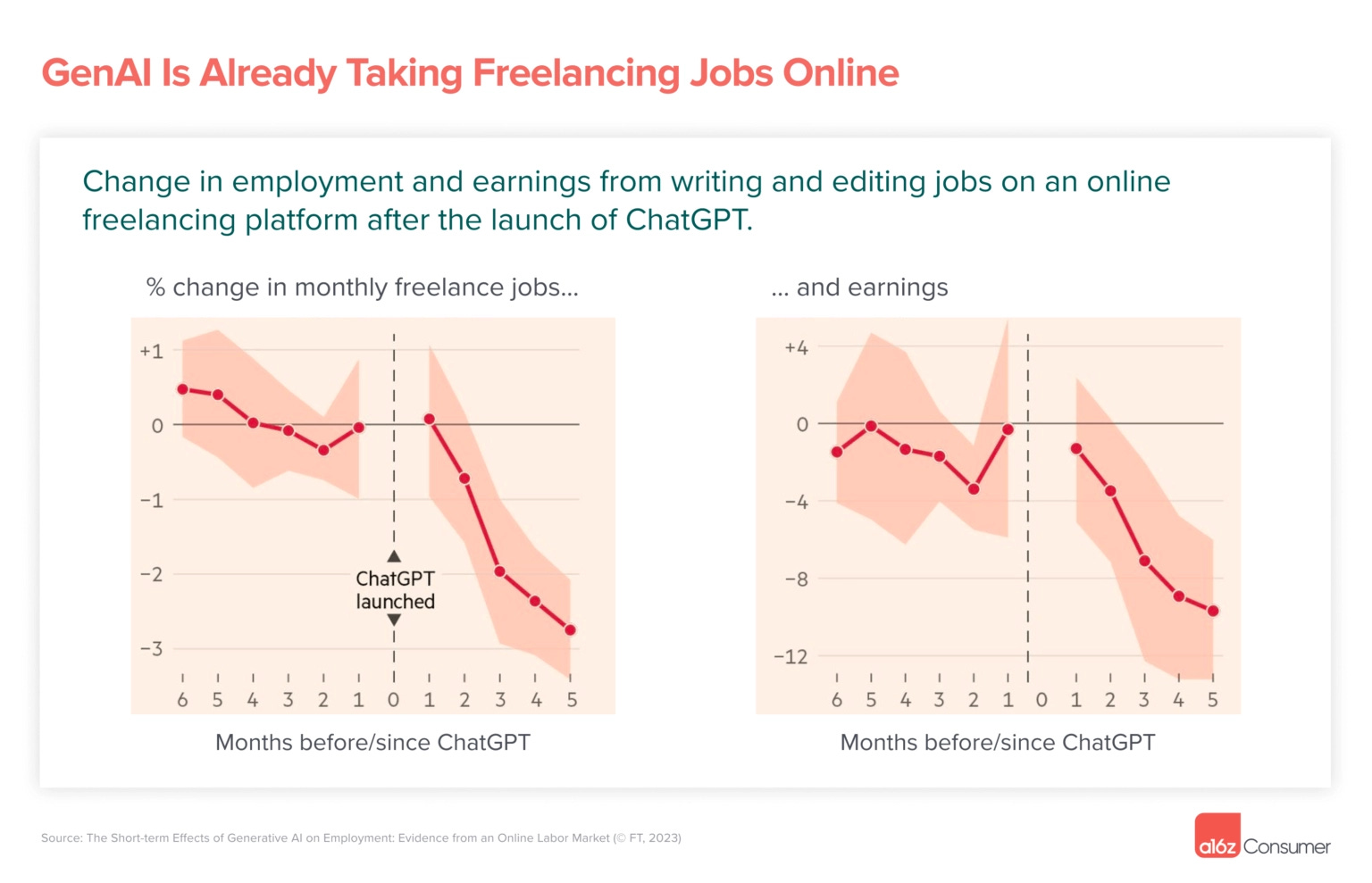

The data seemed to back it up almost from day one. A widely cited Financial Times study of an “online freelancing platform” found that monthly writing and editing jobs fell by about 3% and earnings by about 10% in the five months after ChatGPT launched, as shown below by Olivia Moore at a16z.

{kind=link}

That was 2023, and after this week’s Q1 2026 earnings, I wanted to check whether the assumption still holds.

Before that, a quick macroeconomics detour to set the stage. The headlines have been doom-and-gloom about AI layoffs at big tech companies, but April’s BLS print showed non-farm payrolls up 115K and unemployment steady at 4.3%. The gains were narrow but came from health care, transport, warehousing, and retail. So jobs are still being added on a macro level, just in a narrower, more service-led mix. Those job additions are fully offsetting losses in the tech sector and suggest that, largely, AI isn’t affecting most jobs. It is just impacting those of us who type on a keyboard for a living.

So, how is it going for Upwork?

I jest. 😂

Directionally? Not that bad, actually. “AI eats Upwork” isn’t quite where the numbers land so far.

The Scoreboard

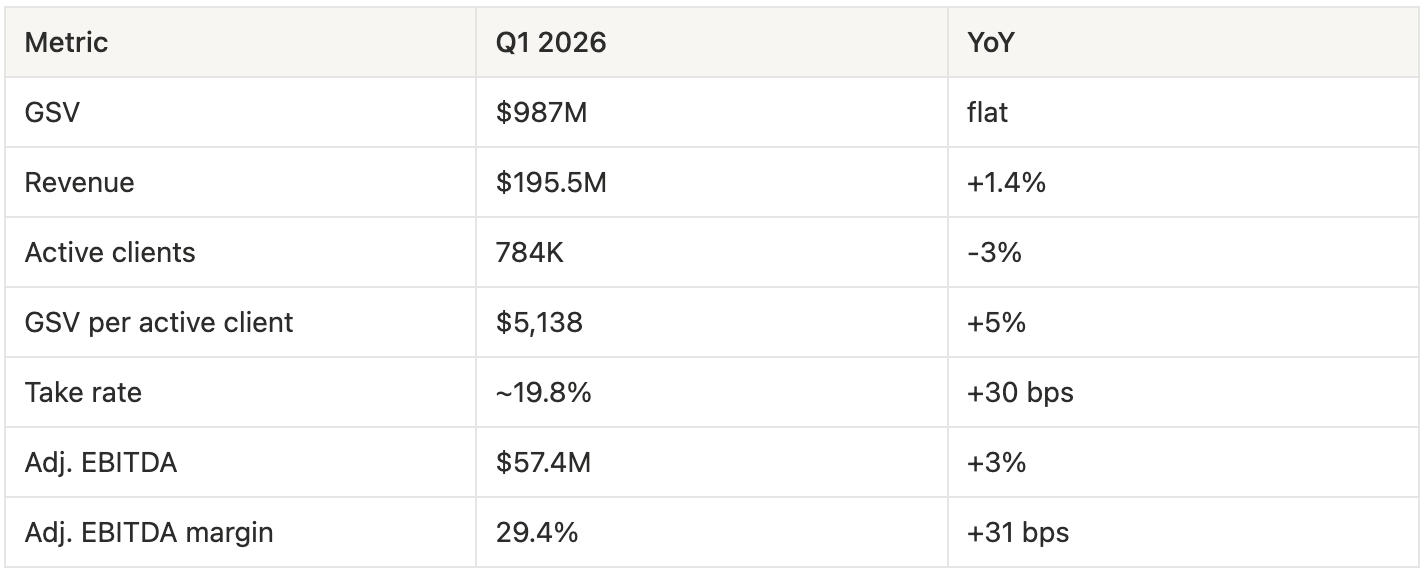

Here’s where Q1 landed for Upwork:

Basically, GSV/Revenue was flat, with active clients slightly down. So, on the surface, things seem soft but okay. Looking under the hood, a few things are going on:

AI-related GSV grew by more than 40% year over year and is now at $300M+ in annualized GSV.

AI Integration & Automation, the biggest AI sub-category, grew more than 50%.

AI work now accounts for about 8% of marketplace GSV (implied).

So demand is not simply going away; rather, the work mix is changing.

Where the Work is Going

CFO Erica Gessert said GSV and active contract trends were “right on plan” through their Q4 2025 earnings call on February 9, then slowed materially from late February through early April, with the greatest pressure on sub-$500 contracts, as customers adopted AI tools to handle the work themselves. The timing lines up closely with the release of Claude Cowork in early January and of Opus 4.6 in early February, among a number of other high-impact releases.

Management never put a percentage on the decline, but you can back into a rough size from the guide cut. The FY26 revenue midpoint came down by ~$67M (~$842M → $775M), which at a ~19.8% take rate implies roughly $340M of GSV that Upwork no longer expects this year. That’s the closest thing to a dollar size on how much AI is impacting the business. A lot of small freelance work is now stuff AI can do well enough.

You might expect freelancers to price their labor lower, given AI substitution, to increase demand, but I don’t think the average Upwork job is getting cheaper. The cheapest jobs are being removed from the platform entirely, or labor is shifting to other roles. Either clients no longer need them, and/or clients are doing them in-house with AI. What’s left, on average, is fewer clients spending more.

Note: Would love for someone at Upwork to validate this!

Product Response

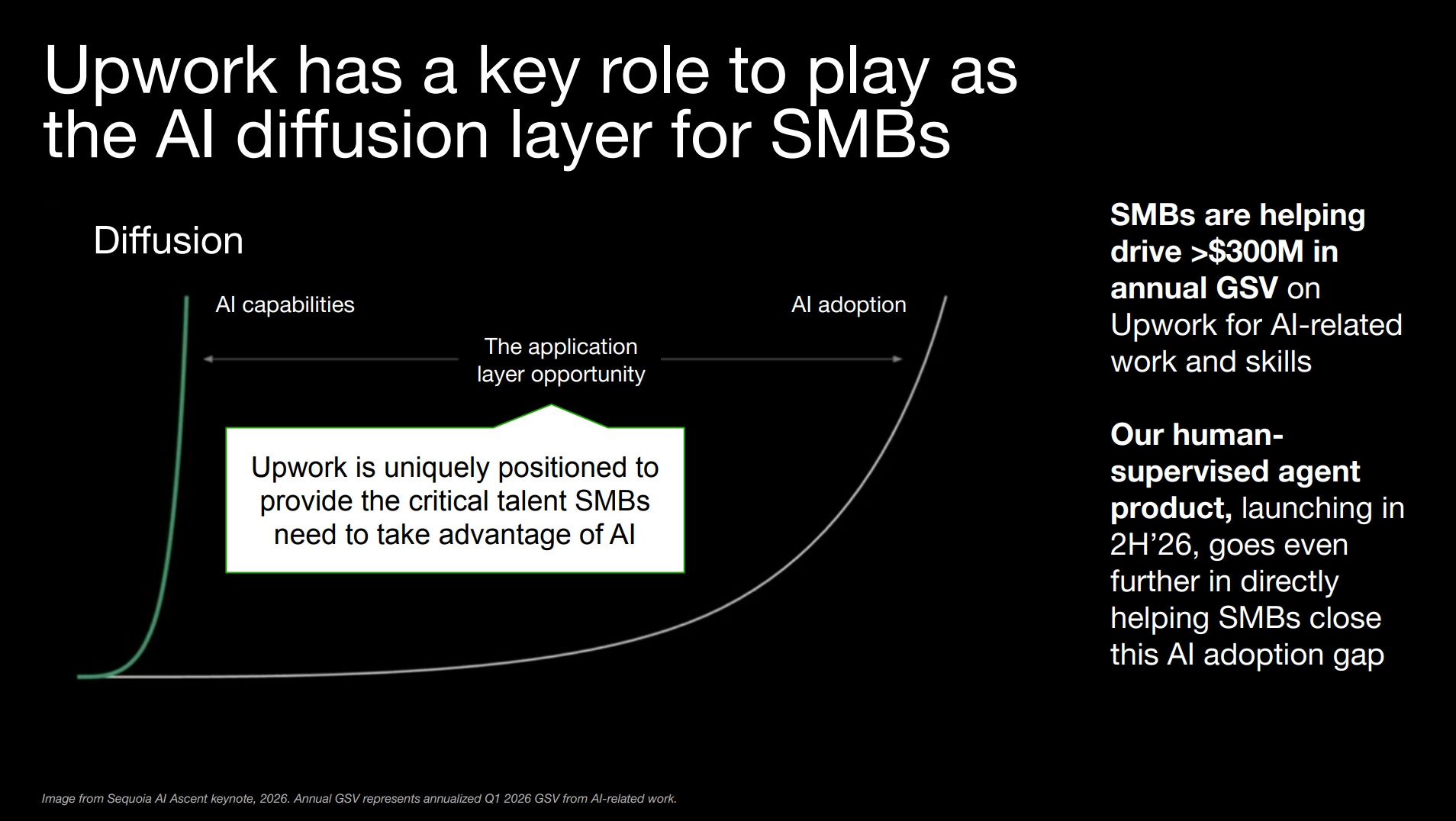

Upwork is obviously working to mitigate the AI pressures, and the shift is showing up in its product roadmap. The bet behind it is simple: AI tools are getting cheaper and more capable, but most small businesses don’t actually know how to deploy them. Upwork wants to be the place where SMBs go to hire AI talent.

Uma, Upwork’s AI assistant for buyers, expanded in Spring 2026 updates with new SMB workflows. They launched an Upwork app inside ChatGPT this quarter, letting a business describe a project, find talent, and draft a job post without ever landing on upwork.com. As many companies are learning, it is now about following the work to where their customers are doing it, which is essentially in Claude and ChatGPT/Codex. Interestingly, a human-supervised agent product goes into beta in Q2, with a broader launch in 2H’26. There are a lot of bets going on, and it will be interesting to see which ones hit. I do think focusing on AI enablement will prove prudent for them in the long run.

The Reset and AI as Aircover

The other piece of the earnings announcement was the layoff. Upwork is cutting roughly 24% of its workforce, with $16-23M in one-time pre-tax restructuring charges, mostly hitting Q2 2026. The reduction in force is expected to remove about $70M of annualized opex from the business, with roughly $40M of that landing in 2026.

The guidance moves alongside the cuts is worth a look:

Revenue: $760-790M, down from the prior 6-8% growth target on FY’25’s $787.8M base, which implied roughly $835-850M.

Adjusted EBITDA: $250-260M, up from the prior ~29% margin target, which on the prior revenue range implied roughly $242-247M. The new midpoint margin is ~33%, and management now expects to hit its 35% adjusted EBITDA margin target in 2H’26, which is more than two years ahead of plan.

A 24% cut framed as “AI-driven” sounds dramatic, but it’s actually a margin reset. So “AI” gives Upwork clean cover for a right-sizing they probably needed anyway (still really sucks for people). The implication is that the same output/EBITDA, maybe more, will come from fewer people. What is different than most companies doing AI layoffs is that AI is actually weakening (and improving) the Upwork business, rather than it being about employees not being needed because of AI (though that could also be true).

Fiverr Cross-Check

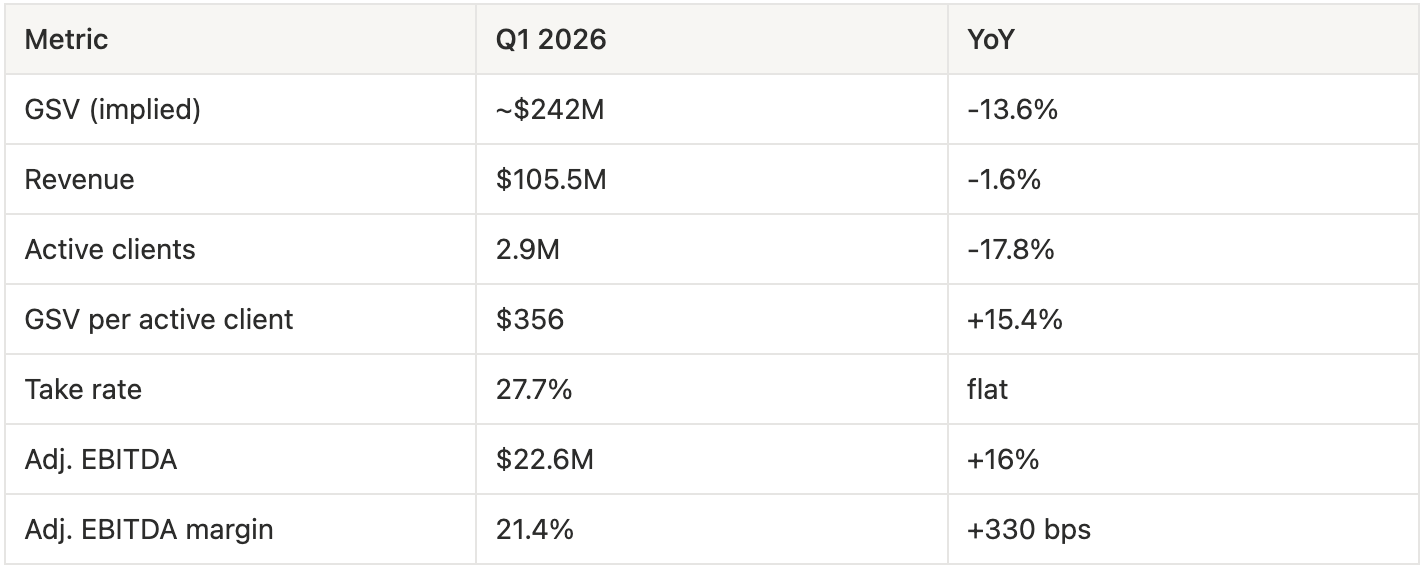

Fiverr reported Q1 2026 a week before Upwork, and the patterns line up almost too neatly.

Fiverr doesn’t publish GSV directly, and the ~$242M is implied from Q1 marketplace revenue ($67.1M) divided by the TTM take rate (27.7%). Active clients and GSV per active client are Fiverr’s annual active buyers and annual spend per buyer, relabeled for parity.

The mix shift is more pronounced than Upwork’s, but in the same direction:

Active buyers fell by almost 18%. That is the cheap-buyer attrition I suspected at Upwork, just much more visible for Fiverr, which has even lower price points.

Spend per buyer is up more than 15%, which is the same survivor-mix story, only more pronounced.

Marketplace revenue is down nearly 14% while services (advertising, subscriptions, etc.) revenue is up 30%. The transactional gig business is shrinking, and the services layer is holding total revenue roughly flat.

Adjusted EBITDA margin expanded 330 bps year over year on slightly declining revenue.

Full-year 2026 guide: revenue reiterated at $380-420M (-12% to -3%), adjusted EBITDA raised to $64-80M (vs. the prior ~18% margin midpoint of roughly $72M). They are also explicitly choosing margin over top-line growth.

The useful thing about looking at the two side by side is what it tells you about the pacing of disruption. Upwork’s numbers look gentler because Upwork is bigger, more enterprise-tilted, and has more mid- and high-value contract types absorbing the shock. Fiverr, which is more concentrated in small, commoditized gigs, is showing the compression earlier and more clearly. Same AI cannibalization either way, but the marketplace labor mix really matters for durability.

In Fiverr’s earnings call, the framing of the strategy was different than Upwork: “from a transactional marketplace to a sophisticated work platform,” with growth coming from “high-value work.” Projects over $1,000 grew at a double-digit rate, and the number of clients completing $1,000+ projects was up 18%. Strip the branding off, and that is similar to Upwork’s “AI diffusion layer for SMBs.” Both companies are conceding that AI is eating the historical core of their marketplaces, and both are trying to graduate to a higher level of the value chain.

Note: Fiverr cut about 30% of its workforce in September 2025, also citing AI.

Conclusion

So is Upwork getting eaten or saved? Both at the same time.

Going back to my original premise, I expected Upwork to be one of the first companies hit hardest by AI. The numbers say I was right about the direction but wrong about the severity, as I missed how quickly demand for AI services would replace the work AI was eating up. Second-order impacts often take longer to show up but can be super meaningful in the long run, which is an important reminder to always think beyond first-order impacts.

The broader read for digital labor marketplaces: the commodity layer is no longer defensible. Anything small, well-scoped, and digital is on borrowed time. What’s most defensible is anything complex, e.g., work that requires expertise and taste. AI services fall into this bucket, and Upwork is betting it can own a chunk of it to drive its top-line growth. It will be interesting to check in on the next earnings report to see how this is all playing out.

Thanks for reading!

Please don’t forget to subscribe and follow me on X and LinkedIn for other great marketplace content. If you’d like to schedule a call, you can find me on expert marketplaces Hubble or Intro.

Power your marketplace with...

Whop Payments Network – Best rates, embedded checkout, global payouts, 24/7 human support, and a whole lot more.

I am thrilled to be partnering with Whop to share an EXCLUSIVE OFFER:

Get your first $200K in volume processed for free.

Accept Card, ACH, Venmo, Crypto, and more with one embedded checkout

Instantly pay out globally in ACH, Venmo, PayPal, & crypto.

Join the network trusted by innovators like Micro1, SideShift, and Metafy.

Learn what the hype is about and claim your benefits here.

About Me:

Colin is a marketplace geek and the General Partner of Yonder, a pre-seed marketplace fund that invests in marketplaces that create new economies. He has also been a longtime advisor to marketplaces, helping them with product growth, monetization, liquidity optimization, and strategy. Previously, he served as the CPO/CRO at Outdoorsy and has worked at Tripping.com, Ancestry.com, JustAnswer, and the Federal Reserve.

Anything small, tidy, and easy to hand over was always going to be the first thing AI made harder to defend.

The work that survives tends to be the stuff that still needs judgement, taste, or someone to sit with the mess properly.

Really appreciate the clarity here on what’s actually happening vs the “AI is coming for everyone” headlines. Human-led, AI-enabled feels like the right direction for any marketplace where the work is high-touch or experiential.