Marketplace Startup Fundraising 2023

Trend data from Carta, marketplace benchmarks from FJ Labs and more!

Hi, it’s Colin from Take Rate. Welcome! I started this newsletter to share startup and marketplace advice for operators by operators. Content is best shared with others, so feel free to share, and if you have any questions, leave them in the comments below!

Update: The Marketplace Startup Fundraising 2025 report is live.

Can we go back to 2021?

VC Friend: Colin, what valuations are you seeing for marketplaces?

Me: Lower…a lot lower

VC Friend: How much lower?

Me: That is a great question! Let me write an article on it.

One clear thing about 2023 is that we aren’t in Kansas or 2021 regarding fundraising. For marketplaces, in particular, benchmarks have shifted dramatically, emphasizing profitable growth and capital efficiency. This is particularly pronounced for marketplaces that typically achieve attractive economics at scale and can require a dump truck amount of venture capital to get there.

Valuations have compressed in the past few quarters, taking its toll. Startups that raised Pre-seed and Seed in the $20-30M+ range (usually a SAFE) and haven’t reached appropriate revenue levels to justify that valuation are experiencing a crunch. This is generally in the form of a bridge or, as it has been rebranded, a “+” round. The tl;dr is that fundraising has become significantly harder because valuations have reset lower, leaving founders to adjust. As always, Bill Gurley captures this perfectly…

I have gotten a front-row seat from both sides of the fundraising process, helping some tremendous marketplace companies raise at valuations they raised at a few years ago. Still, I also have invested in similarly promising companies at very reasonable valuations. The market is in price discovery mode for valuations, and as valuation rigidities shake out, we will see a new equilibrium develop. This will be mean reversion to the long-term growth path of valuations.

Given that backdrop and that I am asked a lot about what I see for marketplaces in terms of fundraising, I wanted to share early-stage data from Carta and some of the benchmarks I often use from FJ Labs to help founders calibrate. I also throw in some of my observations and valuations in the early-stage rounds I am seeing. Hopefully, this can help founders raise better and illuminate for investors what the “market” for marketplace valuations is.

Show me the numbers already!

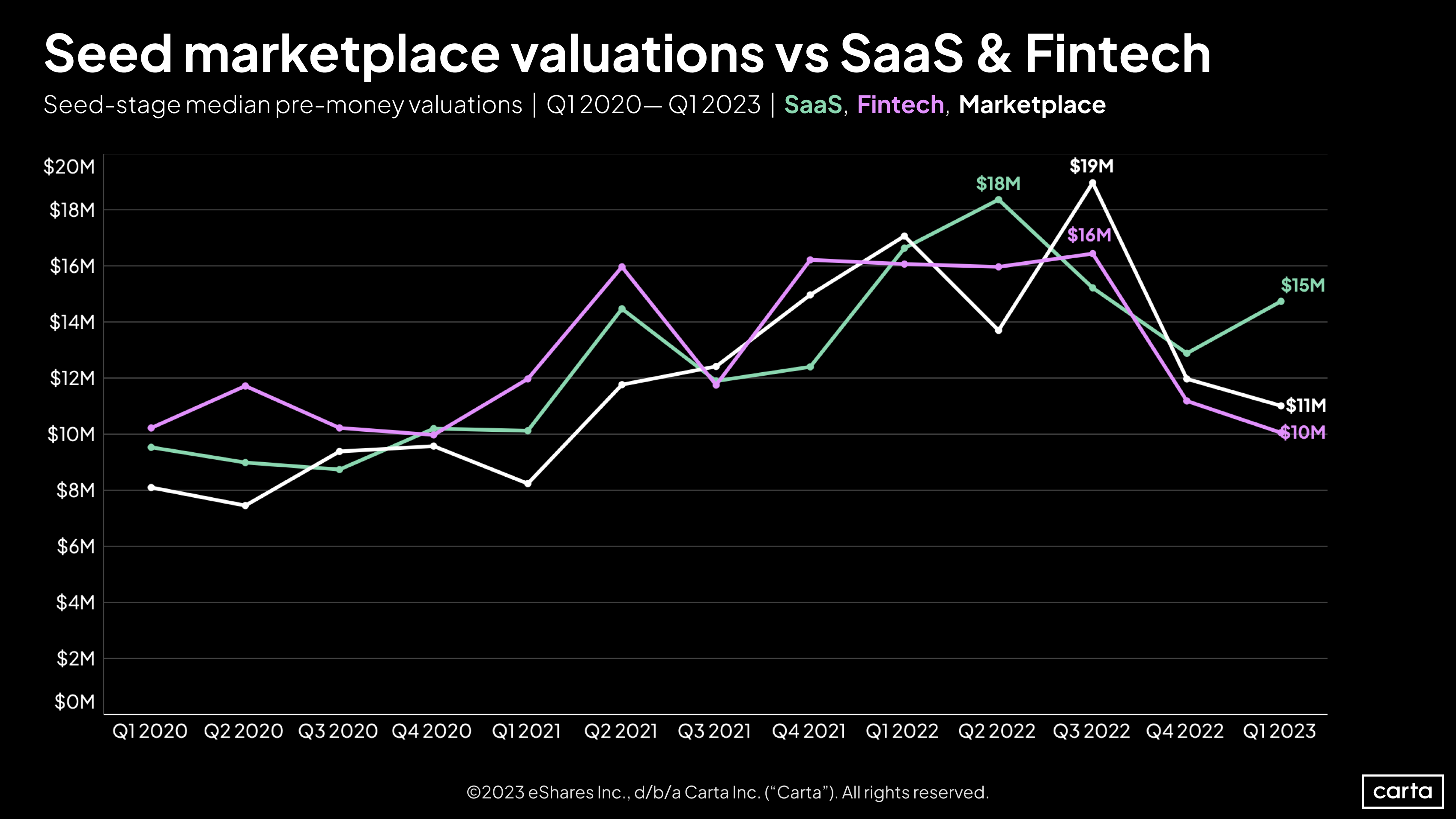

I love data and was super excited to partner with Carta’s Peter Walker on some visualizations of what was happening with marketplace fundraising. In the below charts, we have data through Q1 2023 (my fault for publishing too slowly) showing comparative data between SaaS, Fintech, and Marketplaces at the Seed and Series A rounds. Data was too sparse above Series A to use, which says a lot in and of itself about the temperature in late-stage growth.

If you aren’t already subscribed to Carta’s Data Insights, please do so!

Now to the data! Please note that the data is limited to the companies that use Carta’s software and doesn’t fully reflect the entire funding landscape.

Seed-stage marketplace funding rounds have reflected the slow-down in the macro market, though year-over-year, the number of marketplace fundraising rounds, as measured by Carta, has dropped by ~69% based on deals and appears by even more on a dollar-weighted basis. For comparison, SaaS and fintech deal volume fell ~17% and ~67%, respectively. Lower volume and smaller funding amounts mean lower valuations.

As of Q1 2023, the median pre-money Seed valuation was $11M, down from a peak in Q3 2022 of $19M. Year-over-year valuations dropped by ~35%, with SaaS and fintech falling ~10% and ~37%. Note these are likely lagging in terms of reporting and represent rounds formed earlier in 2022. The current valuations look like a return to those seen in Q1/Q2 of 2021, though not as low as 2020. While the market hit the brakes, the valuations haven’t retrenched fully to pre-COVID levels at the Seed stage.

Let’s see how things look at Series A…

Series A marketplace funding has followed the same trend as Seed but is more pronounced regarding deal velocity, with a ~76% drop year-over-year in reported deals in Carta vs. ~52% and ~41%, respectively, for SaaS and fintech. Marketplaces were hit harder than other categories regarding deal volume, which likely reflects the capital-intensive nature of early-growth stage marketplaces.

Valuations tumbled with the median pre-money Series A valuation for marketplaces at $33M, down from a peak in Q3 2021 of $100M. The $100M peak is likely driven by outlier(s) as the entire cohort of Q3 2021 was only 14 companies, though this is a median and should be a good measure of central tendency. Year-over-year valuations dropped by ~45%, with SaaS and fintech falling ~15% and ~37%.

Interesting to note is that both marketplaces and fintech Series A valuations peaked quarters before SaaS. Deal volume is significantly higher in SaaS, which mutes the volatility in valuations to an extent. What is likely a more significant factor is that many fintech and marketplace companies are B2C, which experienced much swifter valuation compressions as inflation accelerated. The Fed announced its first rate hike in March 2022, the first since 2018.

Another interesting point is that according to the Carta data, Seed valuations didn’t tumble until after Q3 2022, which is well after the peaks in Series A. Given the relative size of funding rounds at Series A and the dour prospects of late-stage funding/IPO for growth companies, the Series A market segment contracted more quickly. The funding velocity at Series B and beyond will continue to be a critical trickle-down for Series A and, ultimately, Seed valuations.

While Carta’s data isn’t a perfect snapshot, it directionally indicates the trending of funded deals. For founders, the tl;dr is that median valuations for marketplaces have at least dropped by ~35-45% across Seed and Series A. Founders must account for this as they look at their next round and adjust expectations quickly.

For example, suppose your Seed was done with a $20-30M pre/post-money cap SAFE, and you are looking at slower-than-expected growth, inefficient spending, marginal unit economics, etc. In that case, you will likely be raising at a flat valuation, if not a down Series A or Seed extension. Remember that the few Series A deals shown in the data set had a median pre-money valuation of $33M, meaning 50% of the deals were below that.

What things did you see in the data that I missed? Be sure to share in the comments!

What are marketplace VCs seeing?

While Carta provides one snapshot of funded deals on their platform, they don’t capture the full spectrum of deals VCs see or the underlying business metrics. Fortunately, Fabrice Grinda of FJ Labs has created and shared what I call the “Holy Grail” of marketplace fundraising. They are a reputable data source and focus predominately on marketplaces. The table I share below is from this post from February 19th, 2021, and is the second iteration, with the first one posted on April 7th, 2020.

Important to note is that the newest table has been updated to reflect the rise of B2B marketplaces with lower average take rates but typically higher GMVs. The numbers provided reflect median ranges, though, as Fabrice notes: “There are many exceptions, especially on the higher end. In other words, the standard deviation is rather high. A second time successful founder can raise at a much higher valuation. A company growing much quicker than the average can often “skip a stage” and have its Series A look like a Series B or its Series B look like a Series C.”

Alright, let’s jump into the data!

First, we can see that Seed and Series A pre-money valuations at the top end of the range align with the reported Carta medians for Q1 2023 at $11M and $33M for Seed and Series A, respectively. For reference, the Q1 2021 reported Carta valuations were $8M and $40M for Seed and Series A. It's not perfect, but it's pretty darn close.

The critical thing to do with this table is to read between the lines. I think the implied growth rates between the rounds regarding net revenue and valuations are the most important to take from the table. Note that the typical timeframe between rounds is 12-24 months, with Fabrice noting 18 months as an implied expectation:

Seed → Series A

Net Revenue (Monthly): 5x

Valuation Step-up: 2.5x

Series A → Series B

Net Revenue (Monthly): 4x

Valuation Step-up: ~2.7x

Series B → Series C

Net Revenue (Monthly): >2.5x

Valuation Step-up: 2.5x

For reference, here is data from Carta on market-wide step-ups between rounds on a post-money basis, which shows similar trends in 2021, though lower step-ups in 2023.

The growth expectations are one of the more critical fundraising puzzle pieces and will largely dictate valuation multiple expansion, assuming all the other parts of the business look good. At the median, marketplaces expecting to move from a Seed to a Series A should have expanded 5X and 4X for Series A to Series B over the last 18 months and expect 1-2.5x multiple expansion. Growth can solve many problems and cover many sins in venture investing.

Some have noted that the FJ Labs data doesn’t reflect the current environment with higher valuations. Still, interestingly, the post was published in Q1 2021, which was also the starting point for the runup in valuations. However, valuations have reset mainly to 2021 levels, suggesting these ranges are generally applicable but likely are only a floor for now, assuming solid economic conditions. The author noted this in response to my tweet (err..xeet?) sharing the table.

Does this table match your experience? Please share your thoughts in the comments.

What is Colin seeing?

My vantage point is a bit different as an advisor to marketplaces, but I have looked at least 200+ marketplace deals (as recorded in my Airtable) in 2023 and actively helped to raise at least ten rounds from pre-seed to Series A (but more towards pre-seed and Seed). Here is my pulse check on what I see regarding funded deals. Please note this is relatively anecdotal.

Pre-seed is largely angels with stage-specific firms doing the top deals and some multi-stage funds in the mix. This reflects a bias towards traction, which means a better risk/reward tradeoff at Seed. Founders with good pedigrees or previous experience are raising as expected.

Seed extensions represent the majority of funding rounds, with many being flat rounds. Traction is emphasized with solid unit economics and scalable distribution. Companies with high-cap SAFEs must get lean and wait for more scale before going to Series A.

Series A is happening, but the goalposts have moved back, with net revenue needing to be over $2M annually and closer to $3M with a strong growth rate and unit economics. Caveats apply for fast-growing companies. The tweet thread with Chris Nakutis Taylor of Nomad Ventures below sums these points up nicely, and a $1M GMV per month for typical marketplaces would imply $1.2-1.8M in net revenue annually.

Series B and beyond have been extremely quiet. Some great companies are growing quietly, though!

If I had to break down valuations for marketplaces in the pre-seed/seed market, here is what I see pre-money:

Pre-product - $3-5M

Post-product and No Revenue - $5-7M

Post-product and Early Revenue - $7-10M

Post-product and Year-ish+ of Revenue - $8-15M

Add $1-2M+ for repeat founders, hot growth, and new vertical

For the VCs out there in pre-seed/Seed funding for marketplaces, I would love to hear if this fits what you are seeing. If you are an AI company, this is all out the window.

Conclusion

To wrap this post up, a lot of data was shared, and I hope it will be of high value to both founders and investors. Multiples have compressed, but the new normal has started to take hold. It is not scientific, but it does feel like markets are thawing a bit. I am cautiously optimistic we will see more later-stage marketplaces and platforms get to IPO in the coming 12-24 months. Instacart will undoubtedly be a start!

Please share your thoughts in the comments. I would love to hear what others are seeing.

Hi Colin! Can you please do a 2024 version of this?

There's a European marketplace startup that raised a $6M Series A round in Q4 2022 but they "only" did $3M in GMV in the whole of 2022 (they expect this to double/triple in 2023). In your opinion, is there anyway this could make sense? Asking because this value is far off the $1M/month GMV before going to Series A that is mentioned above.